Strategic planning with LW·P Lüders Warneboldt

Real estate GmbH

set up - More return,

less risk

Property is a valuable investment with attractive potential returns. A real estate GmbH enables owners and investors to make the most of these opportunities while minimising personal risk. Thanks to tax advantages and a clear limitation of liability, the GmbH offers a solid basis for building up and managing your property assets and protects you from financial risks.

However, setting up a property company is a complex process that requires sound knowledge and strategic planning with regard to company forms and taxation. LW·P Lüders Warneboldt supports you with many years of experience and interdisciplinary expertise at every step – from choosing the right legal form – if it is not to be a GmbH after all – to the tax-optimised structure of your real estate company.

Contact us now for a non-binding consultation and find out how we can support you in setting up your Immobilien GmbH.

What is a Immobilien GmbH?

A Immobilien GmbH is a limited liability company set up specifically for the acquisition, management and purchase of property. It enables property assets to be managed in a structured manner and tax advantages to be utilised.

Why a real estate company for your business succession?

A Immobilien GmbH offers clear advantages for company succession. It separates private and business assets, facilitates the transfer of properties within the family or to third parties and optimises the tax framework.

The advantages of a property company at a glance

Tax advantages:

- Corporation tax: Real estate GmbHs are subject to corporation tax, which is often lower than income tax for private individuals.

- Trade tax: Under certain conditions, trade tax can be avoided or reduced.

- Depreciation: Property even in a GmbH can be depreciated for tax purposes, which reduces the tax burden.

- Avoidance of real estate transfer tax: In certain contribution scenarios, real estate transfer tax can be reduced or avoided.

Limitation of liability:

By establishing a Immobilien GmbH, liability is limited to the company’s assets. This has the advantage that the private assets of the heirs remain protected even if the company encounters financial difficulties.

Professional management:

A Immobilien GmbH enables professional and structured management of the property. This is particularly advantageous when property portfolios are passed on to successors who may not have the same expertise. The GmbH structure also facilitates the financing and management of property projects.

Simple transfer:

The shares in a Immobilien GmbH can be transferred more easily, which simplifies the process of business succession. In contrast to direct property ownership, GmbH shares are more flexible and allow for a gradual transfer of company assets.

Relevant legislation:

Current legislation favours the use of GmbHs for asset management, in particular through reduced tax rates and special regulations for business assets. These legal advantages should be taken into account in succession planning in order to choose the best possible structure for the transfer of the company.

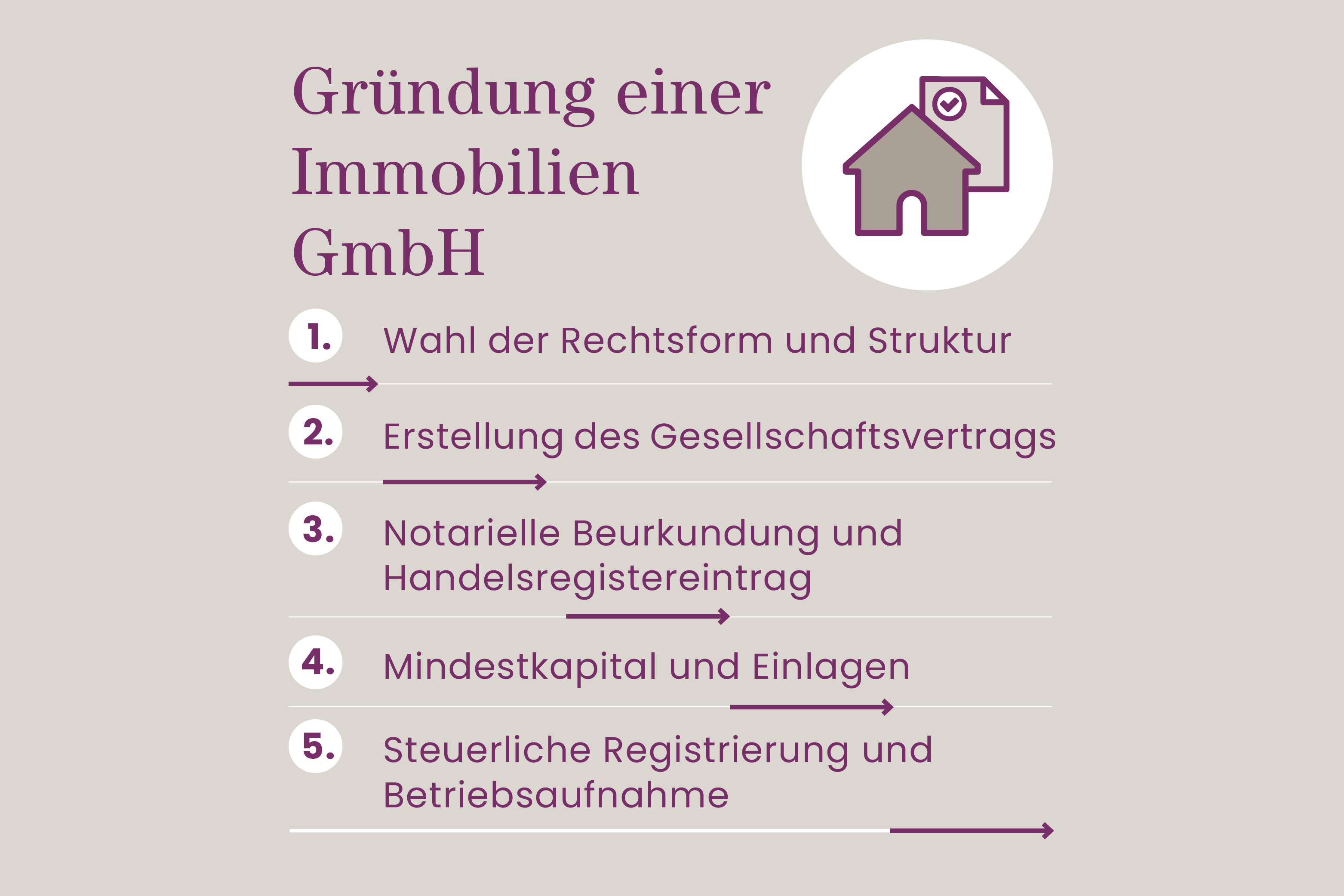

Founding a real estate GmbH with LW·P Lüders Warneboldt - step by step to success

A structured roadmap is crucial for a successful start-up. In the following, we have summarised the key start-up steps and the necessary legal framework for you:

Choice of legal form and structure:

Choosing the appropriate legal form is the first important step. Whether a GmbH or another structure such as a real estate GbR is better suited to your objectives depends on the planned direction of your property company. LW·P Lüders Warneboldt supports you in this decision in order to choose the optimum structure for your project.

Preparation of the articles of association:

A customised partnership agreement forms the legal foundation of the Immobilien GmbH. This agreement regulates the internal processes, the rights and obligations of the shareholders and the management. A detailed and legally compliant drafting of the articles of association is essential for the legal security and smooth operation of the GmbH. Our experienced lawyers draw up this agreement in accordance with the current legal requirements.

Notarisation and entry in the commercial register:

The articles of association must be notarised in order to be legally valid. The GmbH is then entered in the commercial register. Only through these steps does the company become legally capable of acting and obtain its legal status.

Minimum capital and contributions:

A minimum share capital of 25,000 euros is required to establish a real estate GmbH. This capital serves as the financial basis for the company.

Tax registration and commencement of operations:

After entry in the commercial register, the GmbH must be registered with the tax office in order to obtain a tax number. This is necessary for the fulfilment of all tax obligations, including corporation tax, trade tax and VAT. Only after receiving the tax number can the GmbH officially start its business activities.

Also interesting? Read our article on how to set up a GmbH easily from home. (Button on: https://lueders-warneboldt.de/online-gruendung-gmbh/)

Costs and financing of your Immobilien GmbH - transparent and plannable

List of foundation costs

The establishment of a Immobilien GmbH is associated with various costs that should be planned transparently from the outset. The most important costs include

- Share capital: The minimum capital required by law is 25,000 euros, with at least 12,500 euros due immediately upon formation.

- Notary fees: Fees are incurred for the notarisation of the articles of association and other notarial services. As a rule, these are always the same for the formation of a GmbH.

- Commercial register entry: The entry of the GmbH in the commercial register is associated with further costs.

- Consultancy costs: Costs for legal and tax advice, including the preparation of the articles of association by lawyers and tax consultants. If the contract is drawn up by a notary, this does not incur any additional costs.

Running costs and administration

After the start-up, regular running costs arise that need to be carefully calculated:

- Bookkeeping and annual accounts: the legal obligation to keep double-entry accounts and to prepare annual accounts requires regular expenditure on bookkeeping or tax consultants.

- Tax duties: These include corporation tax, trade tax and possibly also VAT, the amount of which depends on the profits and turnover generated.

- Administrative fees: Costs for administrative tasks, such as the management of rental agreements, maintenance and the general management of the GmbH.

Funding and financing options

Various funding and financing options are available for the establishment and operation of a Immobilien GmbH:

- Development programmes from KfW and other development banks: KfW Bankengruppe offers special development programmes for medium-sized companies, which can also be used for real estate GmbHs. These programmes offer favourable loans and grants that can be used to finance real estate projects and secure liquidity.

- Equity and debt financing options: Equity capital can be contributed by the shareholders to strengthen the financial basis of the GmbH. It is also possible to raise debt capital in the form of bank loans or investor participations. These financing options should be carefully analysed and adapted to the individual needs and financial situation of the GmbH.

Taxes and pitfalls with real estate GmbHs

The tax treatment of real estate GmbHs offers both opportunities and challenges.

A Immobilien GmbH is subject to trade tax as it generates commercial income. The assessment basis for trade tax is the trade income, which is calculated from the GmbH’s profit. The tax rate varies depending on the assessment rate of the respective municipality and is generally between 7% and 17%

The profit of a Immobilien GmbH is subject to corporation tax. The current corporation tax rate is 15%, plus a solidarity surcharge of 5.5% on the corporation tax, resulting in an effective tax rate of 15.825%. This tax liability applies to all profits realised, regardless of whether they are distributed or retained in the company.

Inheritance tax is payable on the transfer of shares in a real estate GmbH in the event of inheritance. The shares are valued at fair market value, i.e. the current market value of the GmbH. There are tax allowances and possible reductions, particularly for business assets, which should be taken into account in succession planning.

Real estate transfer tax is payable on the purchase of real estate by a Immobilien GmbH. The tax rate varies between 3.5% and 6.5% of the purchase price depending on the federal state. Real estate transfer tax can also be incurred in the case of certain corporate reorganisations within the GmbH, particularly if there is a change in the beneficial ownership of the property.

The management of a Immobilien GmbH entails increased administrative expenses, in particular due to the obligation to keep double-entry accounts and prepare annual financial statements. This can be a considerable burden, especially for smaller companies.

Tax burden:

The tax burden varies depending on the appropriation of profits and the structure of the GmbH. Profits that remain in the company (are retained) are subject to corporation tax, while distributed profits are also subject to capital gains tax.

Tax rate:

The effective tax rate for profits and distributions can vary. Check the tax implications of each decision carefully and avoid unexpected tax disadvantages.

Our experts at LW·P Lüders Warneboldt will provide you with competent support in all matters relating to the tax planning and management of your Immobilien GmbH. Arrange a non-binding consultation today!

When is a real estate GmbH worthwhile? - Personalised advice for your decision

A real estate GmbH is particularly worthwhile if you manage an extensive property portfolio or generate high sales. Our experts will analyse your individual situation and advise you on the extent to which a GmbH makes sense for you.

Comparison with GbR and sole proprietorship

Compared to a GbR or a sole proprietorship, a real estate GmbH offers limited liability to the company’s assets, which protects the private assets of the shareholders. In addition, GmbHs benefit from tax structuring options that other legal forms do not offer. Our advice includes a detailed comparison of these legal forms to enable you to make an informed decision

Special features of real estate GmbHs

Real estate GmbHs are particularly suitable for managing larger property portfolios, as they offer a clear separation between private and business assets. They allow profits to be reinvested in a tax-efficient manner and offer a structured platform for the professional management and financing of properties.

Successfully founding your real estate GmbH - with the expertise of LW·P Lüders Warneboldt

LW·P Lüders Warneboldt offers comprehensive support in the formation and management of your Immobilien GmbH:

- Advice on formation: We develop a customised strategy for your GmbH and guide you through the entire formation process.

- Tax advice: Our experts optimise the tax framework for your Immobilien GmbH and minimise your tax burden.

- Legal advice: We draw up legally compliant articles of association and offer support with all legal issues.

- Auditing: We examine the financial structure of your GmbH and advise you on optimal financing strategies.

The formation of a real estate GmbH offers considerable advantages, particularly with regard to tax optimisation and limitation of liability. Use the professional advice of LW·P Lüders Warneboldt to find the best solution for you.

Contact us for a non-binding initial consultation. Our experts will be at your side and support you in the successful establishment of your Immobilien GmbH.

FAQ - Your questions about Immobilien GmbH - competently answered

A Immobilien GmbH is particularly worthwhile for investors who own several properties or wish to engage in extensive property trading activities. This legal form offers considerable tax advantages and enables a clear separation between private and business assets. It is ideal for the professional marketing and management of property portfolios. In addition, investors who want to hold and optimise properties in the long term benefit from the legal and tax framework of a GmbH.

A Immobilien GmbH is worthwhile from the point at which several properties are managed or significant rental income is generated. The legal form enables tax optimisation and legally secure structuring of the property assets. This is particularly attractive with increasing property values and an extensive portfolio.

A Immobilien GmbH is subject to corporation tax, which is levied at 15% on the profit. In addition, a solidarity surcharge of 5.5% is levied on the corporation tax. Trade tax varies depending on the municipality and is calculated on the basis of trade income. The effective tax burden can be optimised through various tax planning options, such as the retention of profits.

A Immobilien GmbH is obliged to pay the following taxes:

- Corporation tax: 15 % on the company profit.

- Trade tax: Dependent on the assessment rate of the respective municipality.

- VAT: Is levied on the letting of commercial properties and other services subject to VAT, unless tax exemption applies.

The following requirements are necessary for the formation of a Immobilien GmbH:

- Minimum share capital: 25,000 euros, of which at least 12,500 euros must be paid in immediately.

- Articles of association: Notarisation of a contract regulating the internal structures and shares.

- Entry in the commercial register: Legally binding registration and tax registration with the tax office in order to obtain a tax number.

It depends. A limited company can offer considerable advantages when buying a property. It provides liability protection and offers tax optimisation options. The GmbH can acquire and manage properties for property trading, which is particularly useful for larger investments or complex financing.

Yes, it is possible to acquire a house through a limited company and rent it out to yourself. However, special tax considerations must be taken into account, particularly with regard to the taxation of rental income and utilisation benefits. A detailed tax audit is necessary in order to avoid unwanted tax consequences.