Found a limited liability company: Your comprehensive guide

for a successful start

Establishing a limited liability company (GmbH) is an attractive option for many entrepreneurs. The GmbH not only offers a limitation of liability that protects the private assets of the shareholders, but also a high degree of reliability and flexibility in company management. These characteristics make the GmbH one of the most popular legal forms for companies in Germany.

In this guide, you will learn about the steps involved in setting up a GmbH and the advantages of this legal form. From determining the share capital and drawing up the articles of association to registration in the commercial register – we will guide you through the entire process and show you how to successfully launch your GmbH.

Are you planning to set up a GmbH? Arrange a consultation with our experts!

What is a GmbH - a limited liability company?

The GmbH is a legal form in Germany for companies that value limited liability, reliability and flexibility. It offers:

- Limited liability: The private assets of the shareholders are protected.

- Legal entity: The GmbH acts independently and can conclude contracts.

- Flexibility: Suitable for small and large companies.

The legal framework in Germany

The legal framework for the formation and operation of a GmbH is regulated in the GmbH Act(GmbHG). The most important points include

- Minimum share capital: 25,000 euros, can be contributed in cash or in kind (§ 5 GmbHG).

- Articles of association: Must be notarised and contain essential regulations on organisation and management (§ 2 GmbHG).

- Entry in the commercial register: The GmbH is only legally established when it is entered in the commercial register at the competent local court (§ 11 GmbHG).

- Management: At least one managing director who represents the company externally and manages the business (§ 6 GmbHG).

GmbH Advantages and disadvantages compared

As a legal form, the GmbH has numerous advantages that make it attractive for many entrepreneurs. However, the higher formation costs and the increased administrative burden should not be ignored.

Limitation of liability: The private assets of the shareholders are protected in the event of insolvency or other liabilities.

Reputability and image: The GmbH is regarded as a reputable and established legal form that creates trust among business partners and customers.

Flexibility in structuring: The articles of association and company structure can be customised to meet the needs of the company.

Financing options: GmbHs generally have better opportunities for raising capital than sole proprietorships or partnerships.

Continuity: The GmbH is independent of the shareholders and can continue to exist even if they leave or die.

Tax advantages: Under certain circumstances, tax advantages can arise, for example by retaining profits in the company or by utilising depreciation opportunities.

Formation costs and formalities: The formation of a GmbH is associated with higher costs and formalities than other legal forms. Notarisation of the articles of association and entry in the commercial register are mandatory.

Higher administrative costs: GmbHs are subject to stricter accounting and publicity obligations than sole proprietorships or partnerships.

Double taxation: GmbH profits are first taxed at company level (corporation tax) and then when distributed to the shareholders (income tax).

Stricter regulations: The GmbH Act contains detailed regulations on management, shareholders’ meetings and other aspects of the company that must be complied with.

Our specialised consulting firm will be happy to provide you with comprehensive support for all questions relating to the formation and management of a GmbH. Contact us for a non-binding consultation!

GmbH foundations: The requirements

Before you set out to found your own GmbH, it is important to know and understand the legal requirements. These enable a smooth foundation process and a successful start to your company.

The German Limited Liability Companies Act (GmbHG) stipulates a minimum share capital of EUR 25,000 (Section 5 GmbHG). This capital can be provided in cash or as a contribution in kind (e.g. property, machinery, patents). It is important that the contributions in kind have an appropriate value and are valued by an expert. At least 12,500 euros must be paid in when the company is founded.

A GmbH can be founded by one or more persons (§ 1 GmbHG). These persons can be either natural persons or legal entities. The shareholders contribute the necessary capital and acquire shares.

Every GmbH requires at least one managing director (§ 6 GmbHG). This person represents the GmbH externally and manages the business. The managing director can be a shareholder, but does not have to be. He is obliged to manage the company carefully and conscientiously.

Every GmbH must have a registered office in Germany (Section 4a GmbHG). The registered office is the place where the business of the GmbH is conducted. It must be specified in the articles of association and entered in the commercial register. The business address may differ from the registered office, but must be in Germany and accessible to the public.

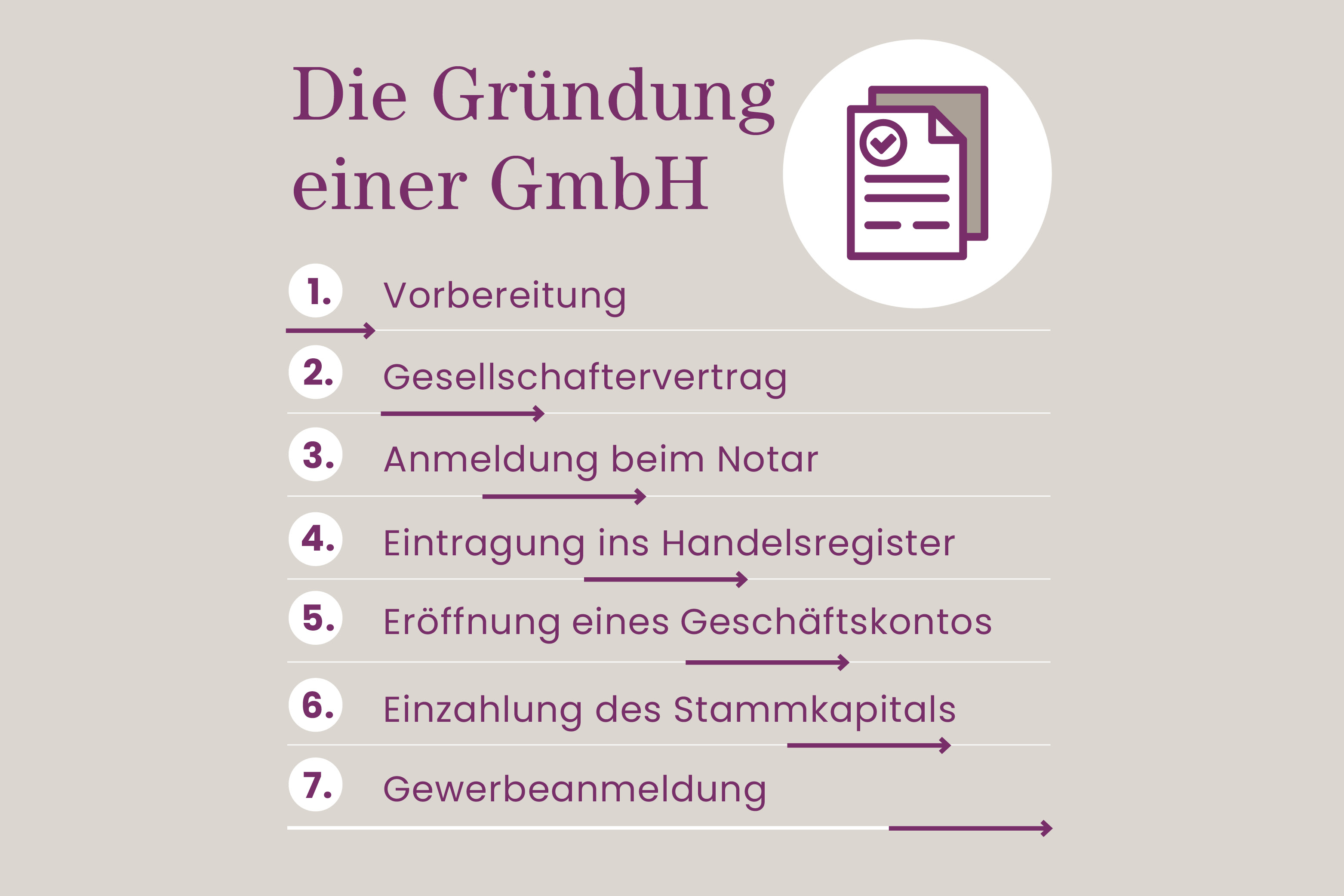

Founding a GmbH: 7 essential steps at a glance

Setting up a GmbH requires careful planning. To give you a clear overview, we have listed the most important steps for you.

1. preparation and planning

Business idea and business plan: Define your business idea precisely and create a sound business plan that sets out your goals, strategies and financial planning.

Advice from experts: Seek advice from experts such as tax advisors and lawyers at an early stage. They can help you choose the right legal form, draw up the articles of association and fulfil all tax and legal requirements.

2. articles of association

Content and design: The articles of association are the heart of your GmbH and regulate the rights and obligations of the shareholders, the company organisation and important aspects such as management, profit distribution and decision-making. Make sure the wording is clear and legally compliant to avoid conflicts later on.

3. formation at the notary

Notarisation: The articles of association must be notarised by a notary. As a rule, the notary drafts or checks the submitted contract for legality and advises you on possible structuring options. Notarisation is a prerequisite for the entry of the GmbH in the commercial register.

4. opening a business account

Choice of bank and documents: Open a business account for your GmbH at a bank of your choice. To open an account, you will generally need the signed commercial register application, the notarised articles of association and the identification documents of the authorised representatives. An entry in the commercial register is not yet required.

5. payment of the share capital

Proof and confirmation: Pay the share capital (at least 12,500 euros) into the GmbH’s business account. Have the payment confirmed by the bank and submit the proof to the notary.

5. GmbH registration and entry in the commercial register

Procedure and documents: Once the share capital has been paid in, the notary registers the GmbH in the commercial register at the relevant local court. As soon as the commercial register has made the entry, the formation of the GmbH is complete.

7. business registration

Registration and authorisations: Register your business with the relevant trade office. Depending on the nature of your business activity, further licences or permits may be required (e.g. trade register, catering licence).

Would you like to set up your GmbH and are looking for competent support? At LW·P Lüders Warneboldt, we are at your side with help and advice. Contact us for a non-binding initial consultation and let us lay the foundations for your company’s success together.

Found a limited liability company: Costs and financing options

The formation of a GmbH involves various costs that you should take into account in your planning.

Start-up costs: What will you have to pay?

Typical start-up costs include

Notary fees: Notarisation of the articles of association is required by law and incurs costs depending on the value of the business. As a rule, the notary fees for founding a GmbH are between 300 and 800 euros.

Commercial register fees: Fees are incurred for the entry of the GmbH in the commercial register. These currently amount to 200 euros (as of 2024).

Consultancy fees: Although it is not absolutely necessary to engage the services of tax consultants or lawyers to assist with the formation, it can be useful. The costs for this can vary greatly depending on the scope of the advice.

Business registration: The costs for business registration vary depending on the municipality and are generally between 20 and 60 euros.

Other possible costs include the creation of a business plan, the opening of a business account, the registration of trade mark or patent rights or the creation of advertising materials.

Financing options: How you can finance your GmbH

There are various ways to finance the formation costs and ongoing business operations:

Equity capital: The equity capital comes from the shareholders and is contributed to the GmbH in the form of capital contributions. This has the advantage that there are no interest payments and the founder retains full control.

Debt capital: Bank loans, loans or investor capital. Borrowed capital can be burdensome due to interest payments and repayment obligations, but offers the possibility of financing larger projects.

Alternative forms of financing

Equity capital: Private investors or venture capital companies can provide capital in return for shares in the company.

Crowdfunding: Financing through many small contributions from a large number of people, often via specialised platforms.

Leasing and factoring: Alternative financing methods to ensure liquidity and finance working capital.

At LW·P Lüders Warneboldt, we provide you with comprehensive advice on all financial and tax aspects of setting up a GmbH. We support you in drawing up a solid financing plan and applying for loans or grants.

Special forms of GmbH: More flexibility for your company

In addition to the classic GmbH, there are also some special forms that may be particularly suitable for certain purposes or types of founders. We will introduce you to the most important special forms and explain their special features, advantages and disadvantages.

The non-profit GmbH (gGmbH) is a special form of GmbH that pursues exclusively non-profit, charitable or ecclesiastical purposes. It is a legal entity under private law and is subject to the German Limited Liability Companies Act (GmbHG) and special regulations on non-profit status.

Special features of the gGmbH:

- Earmarking: The gGmbH may not distribute its profits to the shareholders, but must use them for charitable purposes.

- Tax benefits: gGmbHs enjoy various tax advantages, such as exemption from corporation tax and trade tax.

- Supervision: gGmbHs are subject to supervision by the tax office and possibly other authorities to ensure that they fulfil their charitable purposes.

Advantages and areas of application:

- Tax advantages: The gGmbH offers attractive tax benefits for non-profit organisations.

- Reliability and trust: The gGmbH legal form signals non-profit status and creates trust among donors and sponsors.

- Flexibility: The gGmbH offers a flexible structure for the organisation of charitable projects.

Examples: social institutions, cultural organisations, educational initiatives.

The GmbH & Co. KG is a combination of a GmbH and a limited partnership (KG) and is therefore not actually a GmbH but essentially a KG. The GmbH is the general partner (fully liable partner) of the KG. The limited partners (partially liable partners) can be natural persons or legal entities.

Special features of the GmbH & Co KG:

- Liability: As the general partner, the GmbH has unlimited liability with its assets, while the limited partners are only liable with their liable capital contribution.

- Management: The GmbH usually takes over the management of the KG.

- Flexibility: The GmbH & Co. KG offers a flexible organisation option for the distribution of liability and management.

Advantages and areas of application:

- Limited liability for limited partners: The limited partners benefit from the limited liability of the GmbH.

- Tax advantages: Under certain circumstances, the GmbH & Co. KG can utilise tax advantages resulting from the combination of the two legal forms. Taxation takes place at the level of the limited partners and not at the level of the KG. You look through the company for tax purposes, so to speak.

Examples: Family businesses, medium-sized companies, investment companies.

The Unternehmergesellschaft (haftungsbeschränkt), or UG for short, is a special form of GmbH that is particularly suitable for start-ups with low start-up capital. It is often referred to as a “mini-GmbH” or “1-Euro-GmbH”.

Differences to the classic GmbH:

- Minimum share capital: The UG can be founded with a share capital of just 1 euro.

- Creation of reserves: The UG must allocate at least 25% of its annual surplus to a reserve each year until the minimum share capital of a GmbH is reached.

- Name suffix: The UG must have the suffix “haftungsbeschränkt” or “UG (haftungsbeschränkt)” in its company name.

Formation requirements and advantages:

- Low minimum capital.

- Quick and inexpensive formation.

Disadvantages and risks:

- Obligation to form a reserve until the share capital of the GmbH (25,000 euros) is reached.

- Limited acceptance by business partners.

In addition to the special forms already explained, there are other variants of the GmbH that are tailored to specific needs and applications. Please do not hesitate to contact us if you have any further questions about these special GmbH forms or would like individual advice.

Important legal and tax aspects when founding a GmbH

After clarifying the organisational steps, the focus now shifts to the legal and tax dimension of your GmbH formation.

The GmbH is subject to various types of tax that must be taken into account when it is founded and during ongoing business operations:

Corporation tax: As a legal entity, the GmbH is itself liable to tax and is subject to corporation tax on its profits. The current tax rate is 15 per cent (as of 2024).

Trade tax: The GmbH is subject to trade tax. The amount of trade tax depends on the assessment rate of the respective municipality.

Value added tax: Value added tax is payable on most deliveries and services provided by the GmbH. The standard tax rate is 19 per cent; a tax rate of 7 per cent applies to certain goods and services.

Capital gains tax: Capital gains tax is payable on the distribution of profits to shareholders. The tax rate is 25 per cent plus solidarity surcharge and, if applicable, church tax.

The GmbH is obliged to keep proper accounts and balance sheets. This serves to document business transactions, determine the annual result and provide information to creditors and shareholders. The bookkeeping must comply with the principles of proper accounting (GoB) and can either be done by the company itself or outsourced to a tax consultant.

Since 1 August 2022, the new EU Digitalisation Directive has made it possible to form a GmbH or UG (haftungsbeschränkt) online. The procedure runs via a secure video communication system of the Federal Chamber of Notaries, whereby the notary electronically verifies the identity of the shareholders and notarises the articles of association. This digital option offers flexibility and convenience, especially for founders who want to carry out the process from home.

We have answered the most important questions about online incorporation for you in our article. (Button to the article: https://lueders-warneboldt.de/online-gruendung-gmbh/)

Do you have any questions about setting up a GmbH or the legal and tax aspects? We at LW·P Lüders Warneboldt will be happy to advise you comprehensively and individually. Together, we will find the optimal company form for you and guide you step by step through the formation process. Contact us for a non-binding initial consultation and let us lay the foundations for your company’s success.

FAQ - Frequently asked questions about the formation of a GmbH

The formation of a GmbH often raises many questions. We have compiled the most frequently asked questions from our clients and answered them in a compact and understandable way.

The costs for founding a GmbH vary depending on the individual circumstances. They consist of notary fees for the notarisation of the articles of association, court costs for entry in the commercial register and, if applicable, consulting costs for legal and tax advice. You can find a detailed list of costs in the section “Forming a GmbH: Costs and financing” section of this guide.

To set up a GmbH you need

- At least one shareholder

- A notarised articles of association in accordance with the GmbH Act

- A minimum share capital of 25,000 euros (however, a deposit of 12,500 euros is sufficient)

- A managing director

- A registered office in Germany

There is no legal obligation to set up a GmbH if you have a certain turnover or profit. The decision in favour of the legal form depends on various factors, such as limitation of liability, image, financing options and tax aspects. Seek individual advice to find the right legal form for you.

The duration of the formation of a GmbH depends on various factors, such as the processing time at the notary’s office and the commercial register, the availability of the required documents and the complexity of the articles of association. As a rule, the formation process takes several weeks, but can also take longer under certain circumstances. A GmbH in formation comes into existence upon conclusion of the notarised articles of association.

Yes, it is possible to set up a one-person GmbH. In this case, a single person is both shareholder and managing director.

In principle, any natural or legal person can set up a GmbH. There are no special requirements in terms of age, nationality or place of residence.

At least one shareholder is required to form a GmbH. There is no upper limit for the number of shareholders.

Yes, you can set up a GmbH with 12,500 euros. Although the GmbH Act requires a minimum share capital of 25,000 euros, only half of this, i.e. 12,500 euros, must be paid in before registering with the commercial register.

Yes, it is possible to set up a UG (haftungsbeschränkt), also known as a “mini-GmbH” or “1-Euro-GmbH”, with a share capital of just 1 euro. However, special regulations apply to the UG, such as the obligation to build up reserves until the minimum share capital of a GmbH is reached.