Strategically securing and sustainably shaping your family legacy

Family foundation

Securing and passing on family wealth in the long term presents entrepreneurial families and wealthy private individuals with complex challenges. A family foundation offers a tried and tested means of securing assets in the long term, utilising tax advantages and taking the specific interests of the family into account.

In Germany, the current legal situation supports the establishment of family foundations and opens up a wide range of options for efficient succession planning. It is crucial to analyse the family’s individual goals and needs in order to develop a tailor-made solution.

Contact us for a personal consultation

What is a family foundation? And what goals does it pursue?

Family foundations: Definition, types and delimitation

A family foundation is a foundation with legal capacity under civil law that aims to preserve family assets over generations and to support family members. It can take various forms:

- Pure family foundation: This form focuses exclusively on supporting and promoting the family. This includes financial assistance for the education of children and grandchildren, support for the care of family members and securing retirement provisions.

- Company-linked family foundation: In this case, the foundation’s assets are closely linked to a company, often through the holding of company shares. The main purpose is to organise company succession, keep the company in family ownership in the long term and ensure the family’s financial security.

Example 1:

An entrepreneurial family establishes a family foundation to bundle the company shares and protect them from fragmentation. The foundation distributes profits to the family members, which ensures the family’s financial stability.

Example 2:

A wealthy family sets up a family foundation to manage their property assets. The foundation rents out the properties and uses the income to support the family members, for example for education or care costs.

Would you like to keep your family assets safe and tax-optimised for future generations? LW·P Lüders Warneboldt offers you comprehensive advice on setting up and organising your family foundation.

Purpose of a family foundation

The purpose of a family foundation is defined in the articles of association and primarily serves to preserve the family assets over several generations. This purpose often includes financial support for family members, for example for educational costs or in emergency situations. Another key aspect is to safeguard the family business. A family foundation enables a clear regulation of company succession, protects against the fragmentation of company shares and thus ensures the long-term preservation of the company in family ownership.

The family at the centre: goals and benefits of family foundations

Family foundations serve not only the financial but also the non-material preservation of family assets. They protect the assets from external influences and enable controlled management. In addition to preserving the assets, the focus is on supporting family members, be it by promoting their education and professional development or by providing financial assistance in difficult times.

Advantages of a family foundation: your assets – protected, tax-optimised, sustainable

Family foundations offer numerous advantages that depend on the individual design of the foundation:

Comprehensive asset protection: a family foundation protects assets against unforeseen events such as divorce, insolvency or liability claims. The assets remain in the family and are not fragmented, thus ensuring their long-term preservation.

Tax optimisation: Tax advantages can be used by transferring assets to the foundation. This includes a reduction in inheritance tax through tax-free allowances as well as possible tax advantages in current taxation.

Dual foundation model: The dual foundation model combines a family foundation with a charitable foundation and thus offers special tax advantages. Donations to the charitable foundation are exempt from inheritance and gift tax. This model makes it possible to effectively protect family assets and assume social responsibility at the same time.

Securing company succession: Transferring company shares to a family foundation ensures that the company remains in family ownership and is not fragmented. The foundation’s articles of association can stipulate that the management of the company remains in qualified hands, thereby ensuring the long-term stability of the company.

Strengthening family cohesion: Through joint management and decision-making, family foundations promote cohesion within the family. Members work together to achieve common goals and share responsibility. In the best case scenario, this avoids disputes.

Additional advantages: Further advantages include the reduction of compulsory portion claims, professional asset management and the possibility of also promoting charitable causes.

How to set up a family foundation

Establishing a family foundation is a challenging process. This section provides wealthy private individuals and business families with specific information on setting up a family foundation.

Establishing a family foundation: requirements and legal basis

The first step in establishing a family foundation is to determine the purpose of the foundation and select the appropriate form of foundation. The legal basis is laid down in the German Civil Code (BGB), in particular in Sections 80 et seq. BGB.

The purpose must be clearly defined, legally permissible and achievable in the long term. Typical objectives are the preservation of family assets and the support of family members.

Sufficient assets must be available to fulfil the foundation’s purpose in the long term. The amount of assets depends on the specific objectives and the planned foundation activities.

The foundation requires a board of directors and optionally a foundation council. These bodies are responsible for the management and supervision of the foundation and must have the necessary professional qualifications.

The foundation is established by a written or notarised foundation deed that defines the purpose of the foundation, the foundation assets and the foundation bodies.

Family foundation formation costs

The costs of setting up a family foundation depend on the complexity of the foundation and the assets involved. Initial costs arise from legal and notary fees for drawing up the articles of association and notarising the necessary documents.

Founders should also factor in the fees for official recognition and any costs for the transfer of assets to the foundation. The ongoing administrative costs and expenses for tax advice should also be clarified in advance.

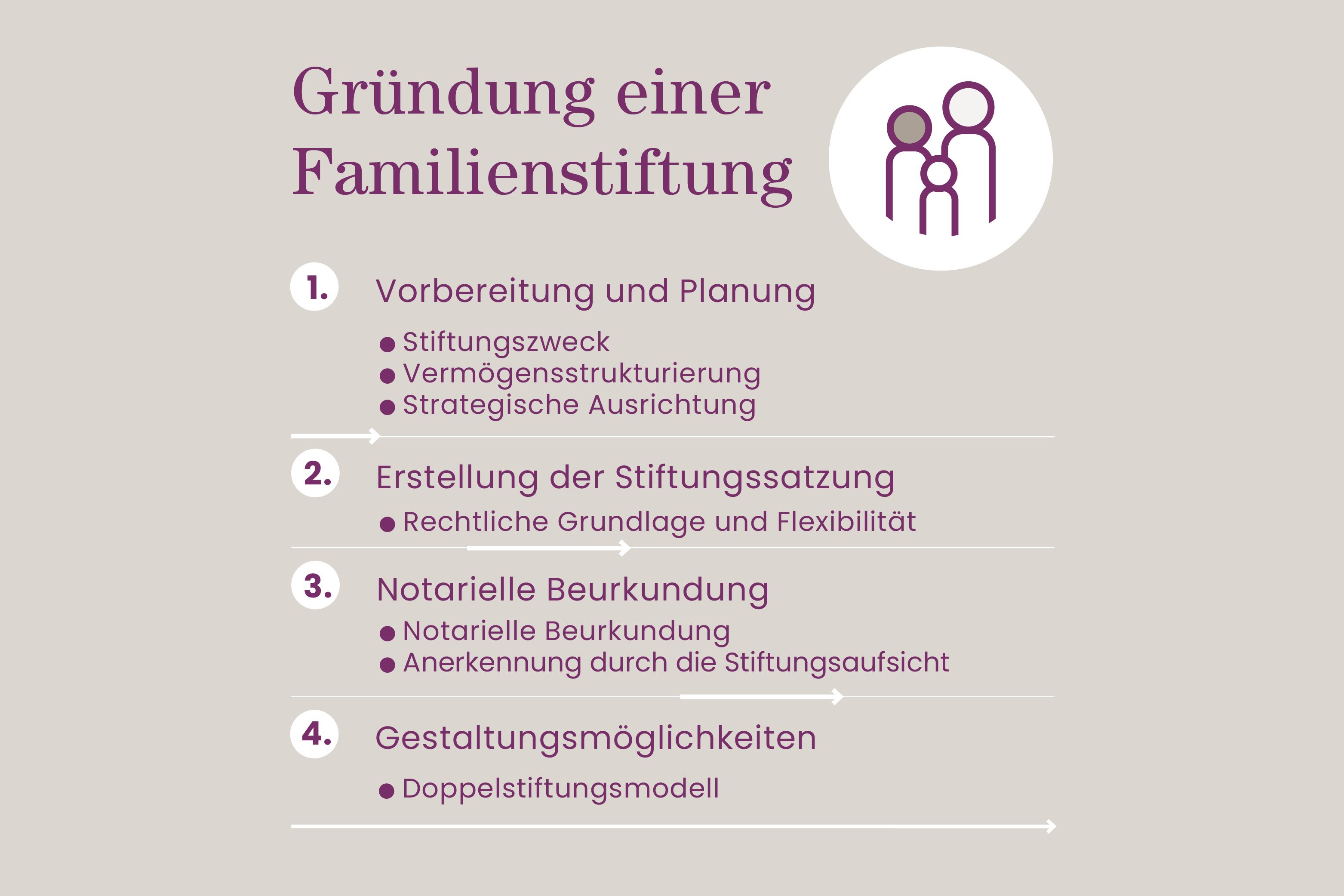

Setting up a family foundation: step by step

1. preparation and planning

- Foundation purpose: Define clearly and precisely what goals you are pursuing with the family foundation. Do you want to secure your family assets in the long term, support your descendants or organise company succession? A clearly defined foundation purpose is the basis for all further steps.

- Asset structuring: Identify the assets that you would like to transfer to the foundation (cash, property, company shares, etc.). Analyse the tax implications of the transfer and optimise the asset structure in order to achieve your goals in the best possible way.

- Strategic orientation: Develop a long-term strategy for the foundation. How should the family assets be managed and increased? What role should the foundation play in company succession? A clear strategy gives your foundation a long-term perspective.

2. drawing up the foundation charter

- Legal basis: The foundation charter is the central document of the family foundation. It defines the purpose of the foundation, the governing bodies (board of directors, foundation council) and the rules for managing the foundation’s assets. Drafting the articles of association requires legal expertise to ensure that they comply with legal requirements and reflect your individual objectives.

- Flexibility: Draft the articles of association in such a way that they also take future changes into account. For example, you can provide for the possibility of bringing additional assets into the foundation at a later date or adapting the purpose of the foundation.

3. notarisation and recognition

- Notarisation: The foundation deed with which the foundation is established only needs to be notarised if shares in a GmbH or real estate are transferred. Notarisation ensures legal certainty and a smooth transfer of assets.

- Recognition by the foundation supervisory authority: Submit the foundation statutes and all necessary documents to the responsible state foundation authority. Once the documents have been checked and recognised by the authority, the foundation is entered in the public register of foundations and thus acquires legal capacity.

4. structuring options

- Dual foundation model: Combine a family foundation with a charitable foundation in order to pursue both private and charitable purposes and benefit from additional tax advantages.

LW·P Lüders Warneboldt accompanies you every step of the way in setting up your family foundation. Contact us for a personal consultation.

Specific use cases: Utilisation of the family foundation for various assets

A family foundation offers flexible options for the structured and sustainable management of various assets. In addition to real estate and shares, company shares, works of art and other valuable assets can also be incorporated. This versatility allows the foundation to be customised to the specific needs and objectives of the family. Specific examples of applications are presented below to illustrate the wide range of possible uses.

Real estate family foundation

A family foundation offers an effective way to secure and manage property assets in the long term. The foundation can act as the owner of the property, which protects the assets from fragmentation. This is particularly relevant if there are several heirs. The rental income can be used specifically to support family members, for example for educational programmes or to secure their livelihood.

Family foundation shares

By transferring shares to a family foundation, the share portfolio can be managed centrally. This enables the shares to be managed professionally and continuously, with the aim of increasing their value in the long term. The income from the shares, such as dividends, can be distributed in accordance with the defined purposes of the foundation, for example to promote the next generation. In addition, the foundation offers a structured framework for the regulation of company succession where company shares are involved.

Taxation of family foundations

How is a family foundation taxed?

The tax treatment of family foundations in Germany is complex and subject to various types of tax. The relevant legal bases can be found in the Inheritance Tax and Gift Tax Act(ErbStG), the Income Tax Act (EStG) and the Corporation Tax Act (KStG). Below we explain the most important tax aspects and current legal situations.

When assets are transferred to a family foundation, gift tax is generally levied in accordance with the provisions of the German Inheritance Tax Act (ErbStG). Family foundations do not benefit from the personal allowances that apply to natural persons. However, when assets are endowed for the first time, they are favoured insofar as the tax class is determined according to the relationship between the founder and the most distant beneficiary. Tax class III is applied to subsequent donations, with a tax rate of up to 50%. There are exceptions for business assets or other favoured assets that fall under Sections 13a, 13b and 13c ErbStG, which offer considerable tax advantages, particularly for large assets over 26 million euros.

After 30 years, the foundation’s assets are subject to inheritance tax, which is levied according to the tax bracket of the most distant relative who is a beneficiary of the foundation’s purpose. This inheritance tax liability can be annuitised over 30 years, with the interest being deductible as business expenses.

Corporation tax: The family foundation is subject to corporation tax. Corporation tax of 15% is levied on the surpluses generated by the foundation. As the foundation itself is not considered a commercial enterprise, it is generally not subject to trade tax unless it maintains its own business operations.

Profits from shareholdings: Profits from shareholdings held by the foundation are also not subject to trade tax. Instead, the company in which the foundation holds an interest is liable for trade tax. This company’s trade tax is not offset against the foundation’s corporation tax.

Family foundations that are commercially active are generally subject to VAT in accordance with Section 2 UStG. This applies in particular to income from the letting and leasing of property and from trading in company shares. However, there are exceptions, such as the VAT exemption for the letting of residential property. The foundation is generally entitled to deduct input tax if it generates taxable sales. A precise examination of VAT liability and a correct declaration are crucial in order to avoid tax risks and secure potential refunds.

The transfer of real estate to the assets of a family foundation triggers real estate transfer tax, regulated in Section 1 (1) No. 3 GrEStG. The tax rates vary between 3.5 % and 6.5 % depending on the federal state. Exemptions from real estate transfer tax are possible under certain conditions, for example in the case of transfers within the family in accordance with section 3 no. 6 GrEStG. However, these tax exemptions are subject to strict conditions and must be carefully scrutinised.

Administration and dissolution of a family foundation

The administration of a family foundation involves the lawful management of the foundation’s assets and strict compliance with all legal and statutory regulations. Protecting the interests of the beneficiaries of the foundation is of central importance. The dissolution process must be clearly regulated in order to protect the rights of all parties involved.

Organs of the family foundation: foundation board and beneficiaries

The central bodies of a family foundation are the foundation board and, if applicable, the executive board. The foundation council is the highest decision-making body and monitors compliance with the purpose of the foundation and the management of the foundation’s assets. The executive board, if present, implements the resolutions of the foundation council and is responsible for operational management.

The Board of Trustees and the Executive Board are primarily responsible for the management of the foundation. The selection of the foundation board and, if applicable, an advisory board is crucial, as these individuals manage the foundation’s assets and ensure that the foundation’s purpose is adhered to. The founder can often reserve the right to manage the foundation as sole director until his or her death. After his death, family members usually take over the board positions.

The beneficiaries are the beneficiaries whose entitlements and rights are defined in the foundation statutes. They have no direct influence on the administration, but are entitled to receive benefits from the foundation’s assets. These may include maintenance payments, educational grants or support for medical needs. The foundation bodies are obliged to use the foundation’s funds in accordance with the defined purpose and to protect the interests of the beneficiaries.

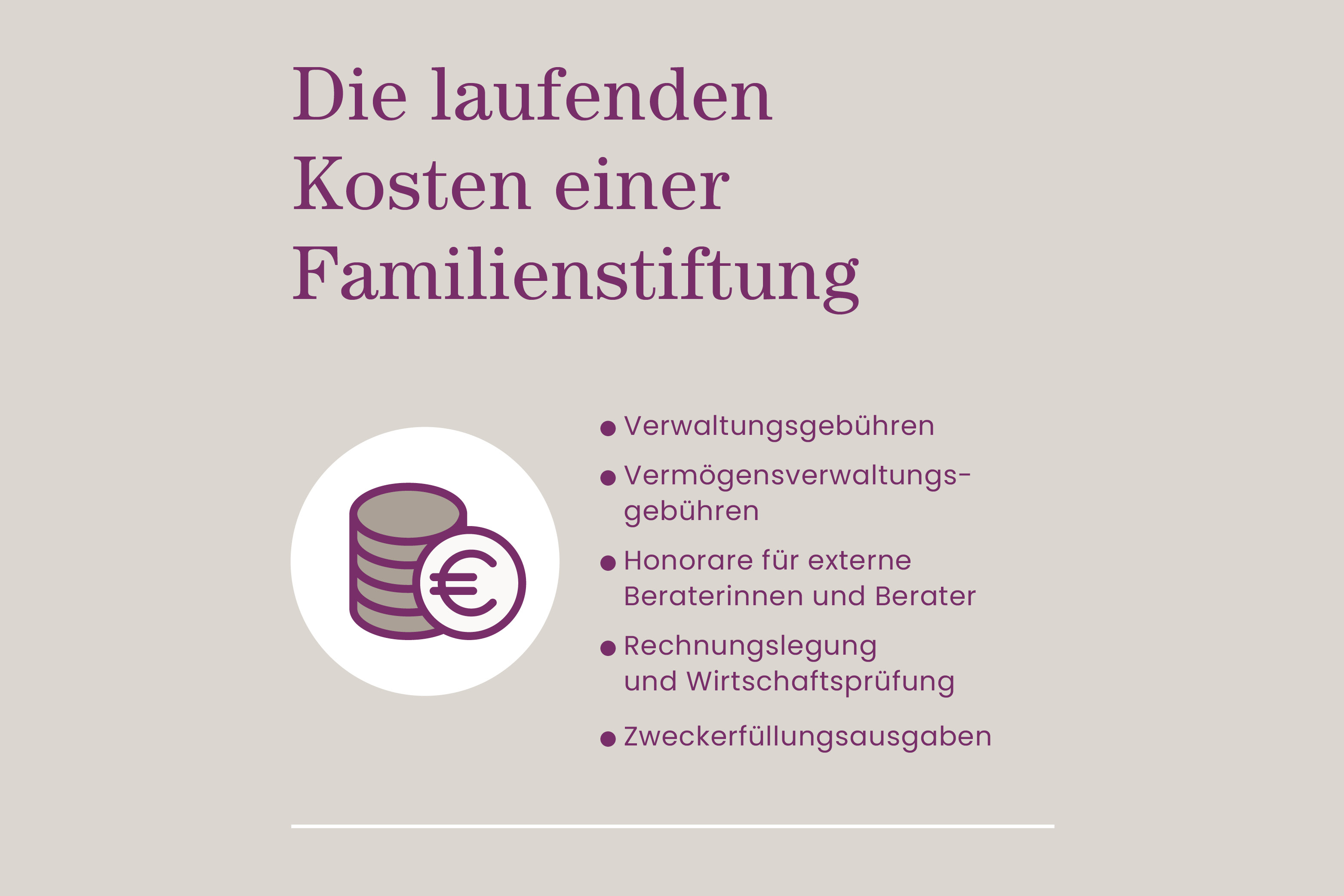

Family foundation running costs: What does the foundation have to pay?

The running costs of a family foundation consist of

- Administration fees: These cover the basic costs of administering the foundation.

- Asset management fees: Costs for the management of real estate, securities or other assets.

- Fees for external consultants: Costs for the services of tax advisors, lawyers and other specialised consultants.

- Accounting and auditing: Costs for the annual preparation and audit of the annual financial statements.

- Purpose fulfilment expenses: Costs to fulfil the purpose of the foundation, such as disbursements to beneficiaries or expenses for charitable projects.

Precise and detailed cost planning is necessary to ensure the financial stability of the foundation. The foundation bodies must ensure that current expenditure is in proportion to income and that the long-term continuation of the foundation is secured.

Dissolving a family foundation: Procedure and consequences

A family foundation can be dissolved when the purpose of the foundation has been achieved, by a resolution of the foundation board or on the basis of a decision by the foundation supervisory authority. The foundation statutes must contain clear provisions for dissolution that fulfil the legal requirements.

The dissolution process begins with an official resolution by the responsible bodies. The foundation’s assets are then liquidated. Firstly, all liabilities are settled. The remaining assets are distributed to the beneficiaries or other authorised recipients in accordance with the provisions of the articles of association and legal requirements.

The legal and fiscal complexity of the liquidation requires a transparent and legally compliant approach in order to avoid legal disputes. The members of the foundation’s governing bodies are responsible for the correct handling of the dissolution and the proper distribution of the assets.

Consultancy by LW·P Lüders Warneboldt

The legal and tax framework for family foundations is subject to constant change. This makes it all the more important to have a reliable partner at your side who closely monitors these developments and offers you sound solutions. LW·P Lüders Warneboldt is at your disposal with a highly qualified team of tax advisors, lawyers, auditors and notaries. We offer you clear, pragmatic solutions that are tailored to your individual requirements.

Expertise in the area of family foundations

Our interdisciplinary team has extensive expertise in all relevant areas and develops customised strategies for structuring and managing your family foundation. We solve complex issues efficiently and work closely with you to take your specific needs into account in the best possible way.

Personalised advice for your foundation

Every foundation is unique. We analyse your situation and develop solutions that are legally secure and tax-optimised. Our advice is precise and reliable, so you can be sure that your foundation is optimally organised.

Arrange a non-binding initial consultation with LW·P Lüders Warneboldt. Our team is at your side.

FAQ - Frequently asked questions on the topic of (family) foundations

A foundation is a legally independent institution that is set up to realise a specific purpose. It differs from associations and companies as it has no members or shareholders. The foundation’s assets are provided by the foundation’s assets and their income. Foundations often serve the purpose of asset protection by securing assets in the long term and protecting them from legal claims.

A family foundation is particularly advantageous if significant family assets are to be preserved and protected over generations. It offers tax advantages, prevents the fragmentation of assets and facilitates succession planning. There is no statutory minimum amount for the foundation’s assets, but they should be sufficient to fulfil the foundation’s purpose in the long term and cover the running costs.

A family foundation is particularly suitable for entrepreneurial families and wealthy private individuals who want to secure their assets across generations. It is ideal for families who want to keep a company in the family for the long term and offers protection from creditors and compulsory heirs. It also serves to provide for family members and takes specific family interests into account.

Funds from a family foundation are paid out to the beneficiaries in accordance with the foundation charter. This can take the form of regular distributions, one-off payments or earmarked support. The amount and type of payments are defined in the articles of association and are based on the purpose of the foundation. It is important that all distributions comply with the legal framework and are authorised by the foundation supervisory authority.

The foundation supervisory authority is a government agency that ensures that the foundation is managed in accordance with foundation law and the statutes. It examines the statutes when the foundation is established, monitors any amendments to the statutes and evaluates the foundation’s annual activity reports. The foundation supervisory authority ensures that the assets are used in accordance with the purpose of the foundation and thus protects the interests of the beneficiaries and the will of the founder.

Yes, amendments to the foundation statutes are possible, but are subject to strict regulations. Amendments must be compatible with the purpose of the foundation and may not significantly change it. The approval of the foundation supervisory authority is required to ensure the legal admissibility of the amendments and to preserve the original intention of the founder.

An international family foundation is established either additionally or exclusively under the law of another country. Such foundations are often used to manage international assets and take advantage of tax benefits in different jurisdictions. When setting up an international family foundation, the specific national laws and international agreements must be observed in order to ensure legal and tax security.